Hi team, My exceptional promise application was rejected with OC2 has approved, I have prepared the following Appeal draft, the assesment panel has overlooked most of the evidence and missunderstood them. My very same MC was accepted last time(November 2025 appeal), I believe my MC and OC3 are actually stronger then accepted oc2 actually(Only my oppinion), OC3 has become stronger than last application(this time startup product launched, got Angel investment interest from UK itself,good traction within 3 months with paying users)

Please look into this,and help me with feedback to adjust this.Thanks

Following is the proforma

following is the current draft I prepared

2.1 (a) Enter the reason for non-endorsement as shown on your decision letter:

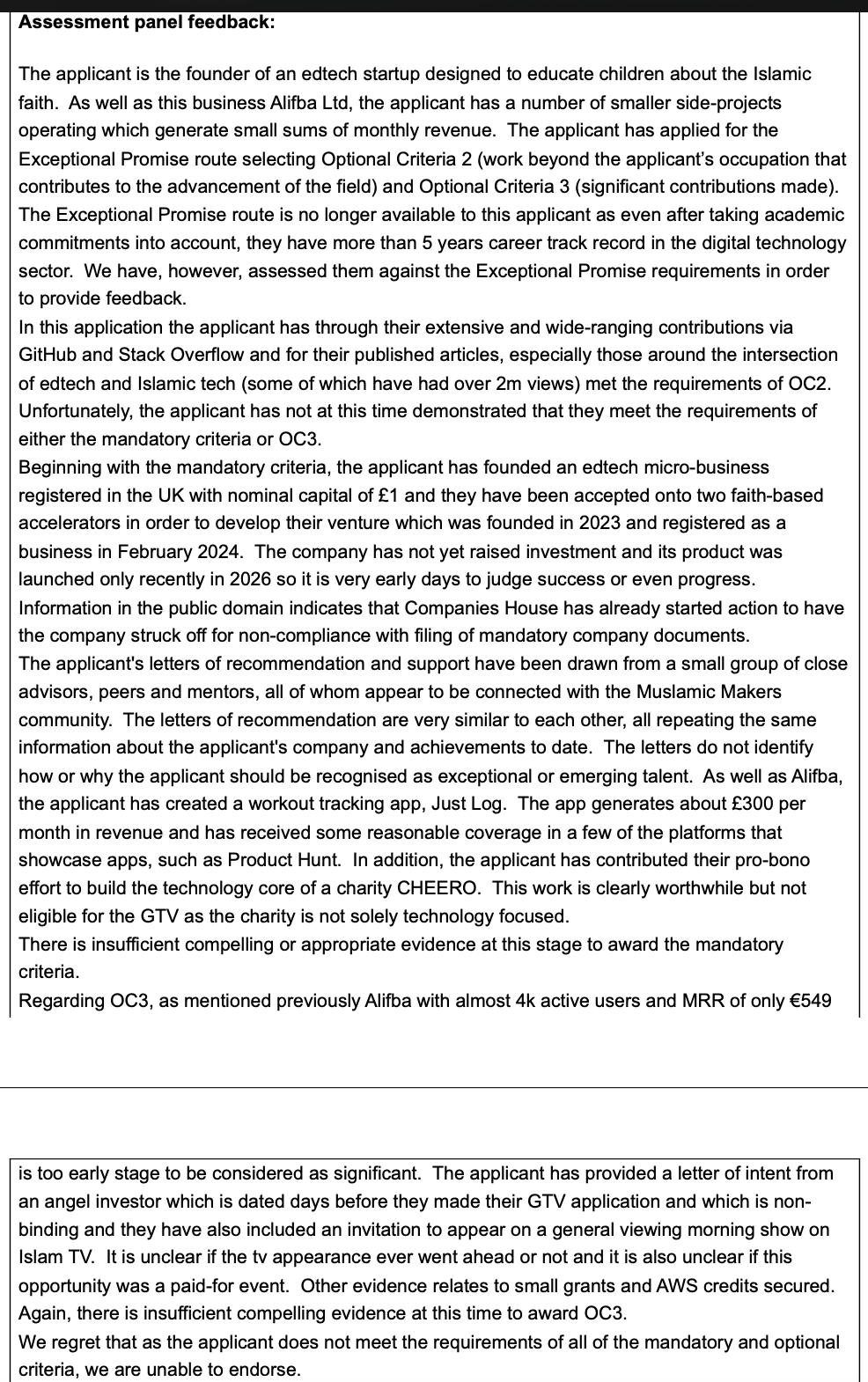

The Exceptional Promise route is no longer available to this applicant as even after taking academic commitments into account, they have more than 5 years career track record in the digital technology sector. We have, however, assessed them against the Exceptional Promise requirements in order to provide feedback.

2.1 (b) Please state in brief terms how you meet the requirement referred to in 2.1(a) and what evidence you provided with your original application to support this:

I sincerely appreciate the panel’s time and careful review of my application. I respectfully submit that certain aspects of my evidence under the Mandatory Criterion may not have been fully interpreted in the intended context, particularly regarding career track record, and forms of external recognition.

The assessment appears to have counted periods that should not be treated as full-time commercial employment in the digital technology sector. They were training, academic, and fellowship-linked activities. The assessment also appears not to have properly paused the career timeline for my full-time MSc Data Science degree from September 2020 to September 2021. This was an academic commitment and should not be counted as full-time commercial digital technology employment. The correct career calculation is therefore materially different.

The following periods should not have been treated as commercial digital technology employment.

- Sept 2017 - May 2018 (8 months): Unpaid undergraduate training at Codemac LLC

- June 2018 - June 2019 (12 months): KSUM Innovation Fellowship

- Sept 2020 - Sept 2021 (12 months): Full-time MSc Data Science

The actual and qualifying paid digital technology career timeline is as follows:

- June 2019 – Feb 2020 (8 months): Junior Android Engineer, Codemac LLC

- Feb 2020 – Apr 2020 (2 months): Android Engineer (Contract), Loud Chilli Media

- May 2022 – May 2023 (12 months): Android Engineer, Intractable Ltd

- Nov 2023 – Present (28 months at submission on March 2026): Founder, CEO & Lead Engineer, Alifba Ltd

- March 2025 – Present: Founder, Indie Hacker, Just Log

So, accordingly, total non-overlapping commercial digital technology experience at application date is approximately 50 months which is 4 years and 2 months. Both Just Log and Alifba are my own ventures, and Just Log overlaps with Alifba and therefore should not be counted separately. On this basis, at the time of my March 2026 Global Talent application, my qualifying commercial digital technology career track record was not more than five years. The conclusion that Exceptional Promise was unavailable to me due to my experience exceeding five years, is therefore a misinterpretation of my academic and professional experience as per my submitted ‘CV.pdf’ document in the application. I represent an emerging technology talent as per the Tech Nation guidelines for Exceptional Promise category.

- The Global Talent route for digital technology is expressly intended for applicants with technical or business expertise in the digital technology sector, including founders, engineers, AI specialists, and those building product-led digital technology businesses.

- GOV.UK confirms that eligible applicants may have technical backgrounds such as developers, engineers, data scientists, or business/product expertise in technology companies that create software, hardware, or process data.

- Tech Nation also distinguishes Exceptional Promise from Exceptional Talent by reference to career stage, with Promise applicants generally having less than five years’ experience and Talent applicants generally having five or more years’ experience.

My application demonstrated a founder-engineer profile. I have built and launched digital products, engineered native mobile applications, integrated adaptive AI systems, achieved recurring revenue, secured competitive accelerator and grant validation, received investor interest, and generated public recognition from product communities, media platforms, and sector-specific networks.

2.2 (a) Enter the reason for non-endorsement as shown on your decision letter:

Beginning with the mandatory criteria, the applicant has founded an edtech micro-business registered in the UK with nominal capital of £1 and they have been accepted onto two faith-based accelerators in order to develop their venture which was founded in 2023 and registered as a business in February 2024. The company has not yet raised investment and its product was launched only recently in 2026 so it is very early days to judge success or even progress. Information in the public domain indicates that Companies House has already started action to have the company struck off for non-compliance with filing of mandatory company documents. As well as Alifba, the applicant has created a workout tracking app, Just Log. The app generates about £300 per month in revenue and has received some reasonable coverage in a few of the platforms that showcase apps, such as Product Hunt.

2.2 (b) Please state in brief terms how you meet the requirement referred to in 2.2 (a) and what evidence you provided with your original application to support this:

I respectfully submit that this section also appears to conflate evidence submitted under the Mandatory Criterion with evidence submitted under Optional Criterion 3. Alifba was submitted principally as evidence of significant founder-led technical and entrepreneurial contribution under OC3, while Just Log and the broader ecosystem recognition evidence were submitted primarily in support of the Mandatory Criterion.

The refusal states that Just Log “generates about £300 per month” and received “some reasonable coverage” on platforms such as Product Hunt. Respectfully, this understates the purpose and significance of the evidence. Importantly, Product Hunt is not simply an app-listing website. It is one of the technology sector’s most recognised product launch and discovery platforms, widely used by founders, engineers, startup operators, venture capital communities, investors, and early adopters to evaluate emerging technology products.

Products do not automatically receive prominent visibility on Product Hunt. Featured products are first selected and surfaced by the Product Hunt platform based on launch quality, engagement, and community traction, after which they compete publicly against other launches through voting and engagement from the wider technology ecosystem.

Just Log was not merely listed on Product Hunt; it was officially featured and subsequently achieved:

- #2 Product of the Day on Product Hunt (Featured)

- #1 Product of the Week in the Health & Fitness category

Product Hunt daily rankings are highly competitive, with large numbers of products launched each day competing for visibility and ranking. Only three products achieve podium placement daily, and featured products are evaluated publicly by a technically sophisticated community consisting largely of founders, engineers, startup operators, investors, and early adopters. In addition, top-ranked Product Hunt launches receive further visibility through Product Hunt’s widely followed daily newsletter reaching hundreds of thousands of subscribers across the international startup and technology ecosystem

The submitted evidence showed that Just Log had:

- over 25,000 total downloads across iOS and Android;

- around 20,000+ iOS downloads;

- around 5,000 Android downloads;

- 4.7-star ratings on both app stores;

This matters because fitness and habit-tracking are among the most competitive consumer app categories, with thousands of established apps, heavy advertising spend, and strong incumbent brands. Achieving this level of adoption, rating quality, and recurring subscription revenue without a marketing budget or team shows genuine product-market validation. It demonstrates that users did not only download the app; they continued to rate it positively, pay for it, and recommend it through organic community channels. Other recognitions that JustLog received include:

- Just Log was also independently recognised editorially by uNeed and selected as one of the ‘Top 10 Best Tracking Products of 2025’. This was relevant because uNeed curates high-quality digital products and software tools for a global technology audience. The recognition reflected independent editorial validation of the product’s usability, design quality, and practical market relevance rather than self-published promotion.

- The product additionally received visibility through F6S, one of the world’s largest startup and founder ecosystems, where Just Log was featured through founder-focused product discovery and startup visibility channels reaching founders, operators, and investors internationally. This extended the product’s visibility beyond ordinary app-store distribution and demonstrated recognition within a broader startup and founder-facing technology ecosystem.

- The evidence further demonstrated measurable commercial and community traction, including recurring subscription revenue, strong public user ratings, significant organic adoption without paid marketing, and substantial community engagement through Reddit, X (Twitter), and build-in-public founder channels.

- Importantly, the growth achieved was entirely founder-led, without employees, external funding, paid acquisition campaigns, or marketing spend. Both Just Log and Alifba were independently designed, engineered, launched, monetised, and scaled by me as a solo founder-engineer. This demonstrates founder-level execution capability across product development, mobile engineering, monetisation, user growth, and operational delivery without reliance on a wider technical team or institutional backing.

Together, these factors demonstrated more than ordinary usage statistics. They evidenced independent market validation, product adoption, founder-led execution capability, commercial traction, and external recognition from users, founder communities, startup ecosystems, and recognised technology discovery platforms.

For the Mandatory Criterion, the relevant point is that a product independently designed, engineered, launched, and led by me achieved measurable external validation and recognition beyond my immediate personal network. This directly supports recognition as an emerging digital technology talent. It shows my ability to independently identify a user need, build the product, launch it, grow it organically, monetise it, and gain visibility in recognised technology communities.

£1 nominal share capital is standard UK startup practice

The reference to “nominal capital of £1” appears to mistakenly imply that the company lacks seriousness or commercial substance.

Incorporating a UK private limited company with £1 nominal share capital is standard practice for early-stage and bootstrapped technology startups. It does not reflect the company’s valuation, product sophistication, founder capability, technical depth, or commercial viability. Incorporation capital was not what I intended to represent through my evidence. I intended to portray and prove that I engineered, launched, monetised, and externally validated a functioning product-led technology platform/

Besides, the venture did not raise institutional capital even earlier because my current UK visa status legally restricts it, which is exactly what led me to apply for a Global Talent Visa, now. Even so, Alifba successfully operated on zero initial capital by securing highly competitive technical grants (ElevenLabs, Deen Developers) and operating as a solo-engineered platform. The venture’s commercial viability has since been formally validated by the £35,000 Angel Investment LOI (at a £700k valuation) and nearly 10,000 initial installs at the time of application.

The refusal says the company had “not yet raised investment” but missed out on assessing the LOI

The refusal states that Alifba had not yet raised investment. However, the original evidence included a £35,000 angel investment Docusigned Letter of Intent at a £700,000 valuation which I received from an established leader in the industry - from Mohammad Shoaib, a London-based Digital Media Executive and Angel Investor, with extensive experience in the global faith-based digital media sector, and someone who has held leadership roles at Muslim Kids TV and Islam Channel. This has been provided on Page of OC3 Company Documents and Investment Recognitions.pdf.

The refusal appears to treat only completed investment as relevant, but early-stage investment pipelines commonly begin with a non-binding LOI before due diligence, term sheet, and final investment documentation. The LOI was therefore evidence of active commercial validation. So, the original £35,000 LOI formed part of an ongoing investment process and continuing commercial discussions.

The “non-binding” criticism misunderstands normal venture investment practice

The assessor appears to treat the non-binding nature of the LOI as a weakness, as though it means the investment was not serious. Respectfully, this misunderstands standard early-stage venture practice. Experienced founders and investors know that investors do not usually sign legally binding investment contracts at the first stage. The normal process is:

- investor interest;

- non-binding LOI or investment intention;

- due diligence;

- term sheet negotiation;

- binding investment documentation; and

- completion.

A non-binding LOI is therefore not evidence of weak investment interest. It is the standard first formal step in an investment process. Every standard Letter of Intent is non-binding. There is also a practical visa-related issue which the refusal does not consider.

The investor could not reasonably bind funds unconditionally before my visa outcome. The investment was linked to my ability to relocate and operate the UK business properly. In commercial terms, the investor was saying: I am prepared to invest if the founder obtains the immigration status needed to build and run the company from the UK.

The refusal therefore creates a logical catch-22:

- The UK-based investor cannot reasonably bind funds before the visa is approved;

- I need the visa to run the UK venture full-time;

- The assessor then discounts the investment because it is not already binding.

This condition does not weaken the LOI. It reflects the commercial reality of investing in a founder whose ability to execute the UK venture depends on the visa outcome.

Mischaracterisation of Accelerator Competitiveness

The refusal describes my accelerator backing as “faith-based accelerators.” This is incomplete and unfairly diminishes their commercial and technical relevance. The evidence did not rely on faith identity as the basis of significance. It relied on competitive entry, founder mentorship, scaling support, technical ecosystem access, infrastructure enablement, and product validation.

The submitted evidence framed these programmes as commercially relevant founder and technology pipelines. They supported the development of a product-led venture and helped validate Alifba’s technical and commercial potential.

The refusal appears to equate a demographic or community focus with a lack of commercial rigour. Specialist founder pipelines can be both community-focused and commercially selective. The relevant question is whether I was selected through a competitive process and whether the programme supported product and technology development.

The evidence showed that Alifba had been competitively selected.

- The Deen Developers evidence letter confirms that my acceptance into the Buildathon was secured from a pool of over 500 applicants, with Alifba placed among the top 20 startups selected. This was not an informal or open-entry activity; selection was based on technical innovation, scalability, and impact. The commercial seriousness of this pipeline is also clear from its alumni outcomes, with startups from the same ecosystem later progressing to globally recognised accelerators such as Y Combinator, including Future Clinic, YC ’24.

- The same applies to the Muslamic Makers Cubit Accelerator. The evidence showed that Alifba was selected into a structured accelerator designed to move technical ideas towards scalable ventures. This was a selective programme, not a casual community event. Its commercial credibility is further supported by the quality of its alumni network, including Anterior, which has raised over US$64 million from leading venture capital firms including Sequoia Capital.

Together, the evidence showed that Alifba had been competitively selected by external startup programmes on the basis of technical merit, scalability, and commercial potential.

Muslim Tech Fest selection was stronger than the refusal implies

The refusal has not fully understood the strength of Muslim Tech Fest London selection. The evidence showed that Alifba was:

- selected from more than 60 applicants;

- one of only five startups to receive a free exhibition slot;

- granted a live demo exception;

- exposed to over 1,800 attendees; and

- presented in an ecosystem associated with major technology supporters, including Google and Amazon involvement.

This serves as startup and technology ecosystem validation. It showed that Alifba was considered sufficiently promising to receive public exhibition and demo visibility in a competitive founder environment. By dismissing these achievements as merely “faith-based,” the assessor missed to evaluate the high technical thresholds required for entry, missing out on my selection into recognized UK diversity and innovation initiatives that routinely produce globally backed startups.

Companies House “Strike-Off” Claim

The assessor claimed that Companies House “has already started action to have the company struck off.” This was an administrative delay, which was the direct result of the UK Government’s recent Economic Crime and Corporate Transparency Act, which requires directors to obtain a personal code using UK biometric IDs. As a non-UK biometric ID holder, I was required to complete alternative verification through an authorised verification provider before filings could be completed.

On re-assessment, it can be noted that the matter has since been resolved and the company remains active and compliant. A temporary administrative filing delay should not reasonably be interpreted as evidence of business inactivity, abandonment, or lack of commercial viability. This is not the same as Companies House initiating a strike-off process for a failed or abandoned company. The current Companies House status can be independently verified here, where the company remains listed as ‘Active’:

ALIFBA LTD overview - Find and update company information - GOV.UK.

The refusal applies too mature a standard to an Exceptional Promise founder

The refusal says the product was launched recently in 2026 and that it is “very early days to judge success or even progress.” This applies a mature-company lens to an early-stage Exceptional Promise founder application. The Exceptional Promise route is specifically intended for emerging leaders and high-potential founders who are still at an early stage of their careers and ventures. The criteria do not require mature-company scale, institutional funding, or large revenue figures. Rather, they assess evidence of trajectory, innovation, technical capability, external validation, and potential to become a future leader within the digital technology sector.

The evidence did not claim that Alifba had already become a late-stage scale-up. It showed strong early-stage progress: product launch, user traction, native app engineering, adaptive AI integration, paid subscription conversion, accelerator validation, competitive exhibition selection, grant validation, investor interest, and recurring revenue. For an Exceptional Promise founder, these are precisely the signals that demonstrate potential, product-led capability, and early commercial validation.

2.3 (a) Enter the reason for non-endorsement as shown on your decision letter:

The applicant’s letters of recommendation and support have been drawn from a small group of close advisors, peers and mentors, all of whom appear to be connected with the Muslamic Makers community. The letters of recommendation are very similar to each other, all repeating the same information about the applicant’s company and achievements to date. The letters do not identify how or why the applicant should be recognised as exceptional or emerging talent. In addition, the applicant has contributed their pro-bono effort to build the technology core of a charity CHEERO. This work is clearly worthwhile but not eligible for the GTV as the charity is not solely technology focused. There is insufficient compelling or appropriate evidence at this stage to award the mandatory criteria.

2.3 (b) Please state in brief terms how you meet the requirement referred to in 2.3 (a) and what evidence you provided with your original application to support this:

The letters were not from a homogeneous peer group but from independent experts across edtech, venture investment, AI/data science, and product leadership, who have addressed different pillars of my profile:

- Shinaz Navas (Ex-Emerge Education VC, CEO) Recommendation Letter 3.pdf, addressed my core engineering capability, evaluating my technical excellence, detailing my architectural discipline, managing parallel native iOS (Swift) and Android (Kotlin) codebases, Ktor backend integration, and the implementation of adaptive learning logic. Shinaz Navas is the Co-founder and CEO of Niyyah, an Islamic education technology platform with over 200,000 downloads, and a former investor at Emerge Education in the UK. He has raised $2.2 million in seed funding for Niyyah and has experience across edtech venture investment, product leadership, and the evaluation of complex education platforms. He is therefore particularly qualified to assess Alifba’s technical architecture, learning design, AI-led education model, and commercial potential within the UK edtech market.

- Assad Masud (CEO, 2M+ users) Recommendation Letter 1.pdf: evaluated my Commercial and Product Strategy. He detailed my product-market fit, subscription conversion metrics, and validated my selection into highly competitive accelerator pipelines. Assad Masud is the CEO of Arabic Unlocked, a digital language-learning platform that has achieved more than two million Google Play downloads. He is therefore directly qualified to assess whether Alifba shows serious edtech product potential, early commercial traction, and founder execution capability. His letter was not casual mentor praise; it was an assessment from an edtech founder who has built and scaled a relevant digital learning product.

- Nima Akram (Staff Data Scientist, Moonpay, Founder: Newscord) Recommendation Letter 2.pdf: spoke about Ecosystem Impact and Ethical AI. detailed my 1.2M+ readership thought leadership, my approach to privacy-preserving AI architecture, and my Stack Overflow engineering contributions. Nima Akram is a Staff Data Scientist at MoonPay, a US-based fintech company, and founder of NewsCord, a UK startup addressing misinformation and bias in news media. Their background includes large-scale transaction data, fraud detection, predictive modelling, machine learning, and product development, and hence qualified to assess my AI, data, mobile engineering, and product architecture decisions, as well as my wider contribution to applied AI and developer communities.

Together the letters triangulated engineering capability, commercial execution, and ecosystem recognition. The refusal appears to have treated overlap in subject matter as repetition, despite the letters evaluating distinct dimensions of the same founder-engineer profile.

Omission of Objective Thought Leadership Metrics

The assessor concluded there was “insufficient compelling or appropriate evidence” for the Mandatory Criterion, but this finding omits my documented thought leadership and its objective global reach. My technical articles on Large Language Models, AI systems and EdTech architecture were published on recognised, Google News-indexed platforms, including Technology.org, which has over 4 million annual readers and a 76+ Domain Authority.

The evidence also included a screenshot/email confirmation from Technology.org’s editorial team stating that my article had generated over 1.2 million views, providing direct third-party validation of readership and reach. In addition, my publication on Influencer Magazine UK independently achieved over 1.9 million verified views.

These are not self-reported claims or ordinary blog posts. They are externally published, technically focused articles with independently evidenced, multi-million readership. Ignoring this publication footprint and its quantified reach is a serious failure to assess objective evidence of emerging leadership, sector visibility and global industry recognition under the Mandatory Criterion.

Misinterpretation of Technology-Led Initiatives (CHEERO)

The refusal states that CHEERO was not ‘solely technology focused.’ Respectfully, this appears to overlook the nature of both the initiative itself and the technology contribution submitted. CHEERO’s publicly described programmes included digital education and computer literacy initiatives, including:

- providing quality education and computer literacy to children and adults;

- free computer courses with qualified tutors;

- internet-enabled educational access;

- and technology-supported learning activities for underserved communities.

My contribution was not ordinary volunteering or administrative assistance. I designed and built ‘CHEERO Connect,’ a reusable full-stack digital platform that supported programme coordination, operational delivery, user management, analytics, accessibility workflows, and telemedicine coordination.

The technology was therefore not incidental to the initiative. It became part of the operational infrastructure enabling scalable programme delivery across education and digital-access activities. The evidence was submitted as an example of technology-led contribution within a digital inclusion and education context, not as general charitable work. The relevant question is whether the work produced substantive digital technology infrastructure with practical deployment and real-world impact. Respectfully, the evidence demonstrated that it did. This can also be independently verified on CHEERO’s website under the ‘Programs’ section, specifically the ‘Education’ subsection, which describes:

- ‘Providing quality education and computer literacy to children and adults’

- ‘Free computer courses with qualified tutors’

- ‘Free library with internet access’

- and technology-enabled educational activities for underserved communities.

The website additionally contains photographs showing active computer literacy classes and internet-enabled learning activities. The organisation was directly involved in digital education and computer literacy, not merely general charitable activity.

For these reasons, I respectfully submit that the Mandatory Criterion was incorrectly assessed. The evidence demonstrated independent external recognition, founder-led technical execution, ecosystem validation, product traction, investor interest, thought leadership with objectively verified readership, and recognition from credible experts within the digital technology sector. The assessment appears to have underweighted or mischaracterised multiple pieces of evidence, applied an overly mature-company standard to an Exceptional Promise founder application, and overlooked the broader context in which the evidence was submitted. I therefore respectfully request that the Mandatory Criterion be reconsidered.